Five-year fixed commercial mortgages all start with the same seed: the yield on the five-year U.S. Treasury note. Forecasts for early 2026 peg that benchmark near 3.0–3.2 percent, so all-in coupons fall into three familiar lanes:

- Moderate credit: 5.75–7.25 percent

- Tight credit: 6.75–8.25 percent

- Easier credit: 5.25–6.25 percent

Want to see the payment and DSCR swing at each rate? Drop the numbers into Lendio’s free commercial mortgage calculator and it’ll do the math for you.

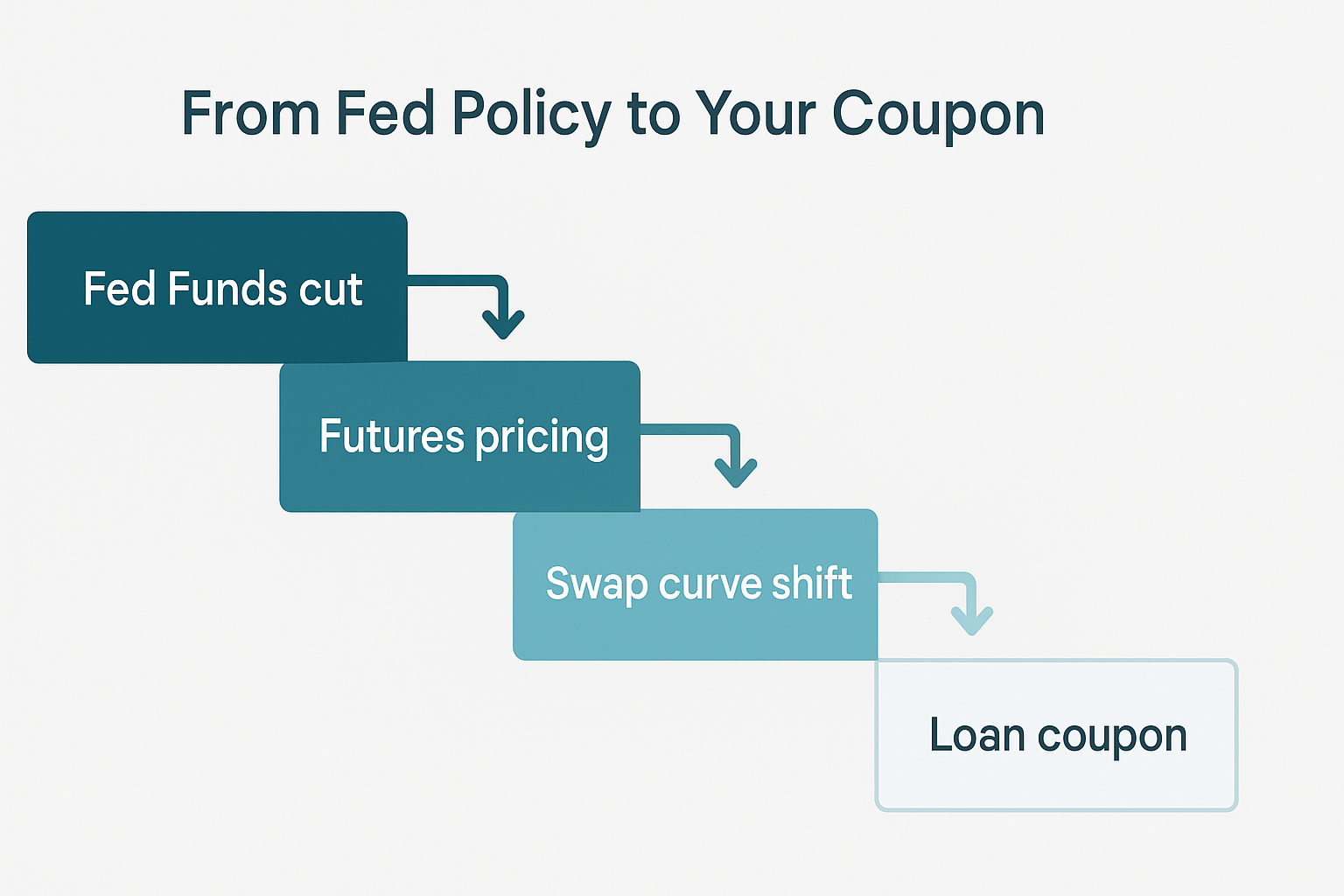

Why the base rate matters

Every five-year fixed quote begins with one figure: the yield on the five-year U.S. Treasury note.

When that yield slips, lenders fund more cheaply and pass part of the savings to you. When it climbs, wider spreads can’t fully cover the jump, so the all-in coupon still moves higher.

Policy shifts flow straight into that number. Federal Reserve rate cuts first show up in futures, then in swaps, and finally along the Treasury curve. Balance-sheet runoff (quantitative tightening) drains cash from the bond market and often adds a few basis points to term premiums when liquidity thins, according to the St. Louis Fed (stlouisfed.org).

Volatility counts as much as direction. During the April 2025 sell-off, the 10-year yield swung 47 basis points in a single week, a 99th-percentile move in modern trading history, according to the St. Louis Fed.

Because the five-year Treasury trades in real time, it offers a cleaner signal than any static rate table. Keep that quote window open; it can tell you more about tomorrow’s term sheet than last night’s mortgage grid. An online commercial mortgage calculator converts each basis-point shift into a clear monthly payment and total-interest figure, so the impact lands in dollars, not decimals.

Credit-spread wildcards

Treasury yields set the floor, but credit spreads decide how high you jump.

Three forces are keeping that premium wide as we move toward 2026:

- Basel capital redo. According to Reuters, U.S. regulators aim to unveil a more “industry-friendly” Basel III Endgame draft by early 2026, yet banks expect higher risk-weighted assets and are padding spreads until the text is final.

- Market stress. Office loans in CMBS reached an 11.08 percent delinquency rate in June 2025, while special servicing across all property types stayed above 10 percent, conditions that push conduit bond spreads—and loan coupons—higher, according to CREFC.

- The maturity wall. About 533 billion dollars in commercial mortgages mature in 2025, crowding the hunt for refinancing dollars and giving lenders room to widen spreads, especially on loans above 65 percent loan-to-value, according to Trepp.

Together, these wildcards can tack on 100 basis points or more to an otherwise friendly five-year Treasury quote. Track them weekly; a 5.9 percent wish can quickly become a 6.9 percent reality.

Capital-source cheat sheet

Lenders aren’t interchangeable. Every capital pool follows its own rules and risk limits, so two term sheets for the same property can differ by a full percentage point. To see those gaps side-by-side, many borrowers now start with an online commercial-loan marketplace such as Lendio, which forwards one application to a network of 75-plus bank and non-bank lenders and returns competing term sheets within days.

Bank and credit-union balance-sheet loans

For small and midsize deals, the local bank is often the first stop. Because the loan stays on the lender’s books, regulators and deposit flows set the price.

- Typical structure: five-year fixed rate, 25-year or 30-year amortization, with a balloon at year five. The Office of the Comptroller of the Currency (OCC) labels this a “standard” real-estate term loan.

- Pricing: At ≤65 percent loan-to-value (LTV) and a stressed DSCR above 1.35×, coupons usually land near the low end of the base-case range.

- Flexibility: Banks can add recourse, cross-collateral, or cash management to clear credit boxes. Many will trade yield maintenance for a three-percent declining prepay.

- Call risk: If credit conditions tighten or Basel capital updates add weight, renewal isn’t automatic. Build an exit plan early; paying down principal often beats an extension fee.

How property type and LTV shape your 2026 coupon

Lenders size up risk through two fast lenses: what the building is and how much debt sits on it. Those inputs set the coupon long before anyone debates paint colors.

- Multifamily and industrial. Stable rent rolls and strong demand make these the honor-roll assets. At ≤60 percent LTV, recent five-year fixed quotes have cleared in the low-five-percent range, according to CBRE’s Q1 2025 lending survey, where multifamily spreads averaged 149 bps over Treasuries.

- Grocery-anchored retail. Essential-needs traffic keeps cash flow sticky, but headline retail worries add a modest premium, typically 20–40 bps above comparable multifamily debt in the same market, according to CBRE’s H1 2025 cap-rate survey.

- Non-grocery retail and hotel. Seasonal cash flow and shorter leases widen spreads. Even at 55 percent LTV, recent executions land in the mid-six-percent bracket when the five-year Treasury sits near 3 percent.

- Office. Vacancy risk and heavy cap-ex make most lenders cautious. A top-tier office at 45 percent LTV can still price above 7 percent, while anything riskier moves into the tight-credit band.

The pattern is simple:

- Safer assets earn the tightest spreads.

- Every 10-point rise in LTV adds roughly 25–50 bps.

- Risk premiums stack; a high-LTV office refinance faces two headwinds, not one.

Plot your property on that grid before you sign a term sheet, and you’ll know at a glance whether the offer feels generous or grim.

Underwriting levers you control

Rates move with the market, but underwriters still give you five knobs to turn.

- Debt-service coverage (DSCR). Banks usually stress the rate by 100 bps and look for at least a 1.25× cushion on income-producing properties, per FDIC examiner guidance. Raise NOI or borrow less and the spread tightens.

- Loan-to-value (LTV). Every notch below 65 percent reduces loss severity, so lenders sharpen pencils. A last-minute equity boost today can save years of extra interest.

- Lease rollover. When more than 20 percent of rent expires before the balloon, pricing widens. Staggered, longer leases reassure credit committees—and you.

- Sponsor strength. Ample liquidity and clean global cash flow signal that you’ll write the check if the roof leaks. Weak guarantors add basis points.

- Property condition. Deferred maintenance unnerves appraisers. Fix obvious issues before the site visit and you earn credibility no spreadsheet can replicate.

Tuning even one of these levers can shave 25–50 basis points off the final quote.

Lock, float, or swap?

Rates move, but fees stay put. Here’s how each choice usually plays out:

- Lock. Paying 10–20 basis points up front can freeze your coupon for 30–60 days, according to MBA closing-cost surveys. If you’re closing within two months and the five-year Treasury trades inside its recent ±15 bp band, lock when you sign the term sheet.

- Float. You skip the lock fee and gamble on every CPI release. A 25 bp market pop on a five-million-dollar loan adds about 10 000 dollars a year in interest.

- Swap. Converting a floating note to a fixed swap delivers full-term certainty, but prepaying early can trigger a make-whole equal to the present value of the foregone interest, so estimate that cost before you commit.

Rule of thumb: If a Fed meeting lands before your closing and traders expect a cut, you can float to the decision—just keep a lock order ready. If you plan to hold through full amortization and dislike balloon risk, the swap may be worth the discipline despite the exit penalty.

The 2026 refinance crunch

Think of the 2025–26 maturity wall as a long security line with too few agents. Trepp estimates about 533 billion dollars in commercial mortgages will come due in 2025 alone. Not every loan will find a fresh lender.

Underwriters will triage by asset quality and sponsor strength. Class-A multifamily at modest LTV jumps to the front, while a half-empty mid-tier office moves to the back, often at a higher spread.

If your note matures within 18 months, move early:

- Update the numbers. Order current financials and clean the rent roll.

- Plan for equity. Budget a 10–15 percent pay-down to turn a maybe into approved.

- Start talks early. Open lender conversations at least nine months out since third-party reports and committees eat weeks.

When options narrow, plan B beats panic. A short-term bridge or partial defeasance can buy time and costs less than a fire-sale discount or handing back the keys.

Case studies

Owner-occupied SBA 504 blend

Maria runs a specialty-coffee roastery in Denver. She’s buying a three-million-dollar warehouse, adding light tenant improvements, and wants rate certainty for five years without draining cash.

We structure a classic SBA 504:

- Bank first lien: 65 percent of purchase, five-year fixed, 25-year amortization.

- CDC debenture: 35 percent, fully amortizing 25-year note. February 2026 debenture pricing printed at 5.90 percent, down from 6.02 percent in late 2025.

The bank slice tags on 3.10 percent (five-year Treasury) + 240 bps, for an all-in 5.50 percent coupon. Blended across both liens, the weighted rate is 5.68 percent.

Monthly payment (estimated with a mortgage calculator): 18 740 dollars

Projected NOI (year 1): 32 900 dollars → DSCR: 1.76× after a 25 bp stress bump.

Key take-aways:

- The CDC’s longer amortization softens payment shock, so higher debt still pencils.

- The first lien balloons in year five, giving Maria the option to refinance that slice if base rates fall.

- Equity outlay stays below 10 percent after closing costs, freeing cash for roasting equipment instead of fees.

Bottom line: An SBA 504 combo can deliver life-company pricing with community-bank flexibility, a playbook owner-users can trust for stability in 2026.

Conclusion

- Match the lender to the deal. A 60 percent-LTV industrial building belongs on a life-company desk, not in a community bank inbox. A value-add neighborhood retail strip with mom-and-pop tenants is pure local-bank territory. Fit matters; scatter-shot requests waste time and signal desperation.

- Package the file like a credit officer. Most banks expect three years of operating statements, a current rent roll, guarantor financials, and a two-page memo that covers the problem, the solution, and cash-flow proof. This checklist mirrors the MBA’s 2025 loan-application survey, so deliver it up front and you’ll skip weeks of back-and-forth.

- Pull at least two shadow bids. A life-co quote keeps your bank honest on spread, and an SBA 504 term sheet gives you backup if amortization needs a boost.

- Set a firm timeline. Tell every lender when you’ll choose a term sheet and stick to it. A clear deadline bumps your file up the stack and filters out desks that can’t deliver.

A focused RFP beats a fishing expedition every time. You’ll land cleaner terms and close faster, with fewer bruises to show for it.

FAQs

Q: Why do UK comparison sites appear when I Google “commercial mortgage rates 5-year fixed”?

Ans: The phrase is common in British lending, so Google mixes U.K. pages into U.S. results. Skip pages quoting sterling or Bank of England rates; focus on sites that mention the five-year U.S. Treasury and price in dollars.Q: Can I get a true 30-year fixed rate on a commercial property?

Ans: It’s rare. Only agency multifamily programs, such as Fannie Mae’s fixed-rate DUS loans, stretch to thirty years, and they limit both property type and loan size. Most other commercial lenders offer five- or ten-year terms with balloons.Q: Why are commercial rates higher than residential mortgages?

Ans: Commercial loans carry business risk, vacancy exposure, shorter amortization, and higher capital charges. Without government backstops like Fannie or Freddie, lenders price a wider spread over Treasuries to cover that risk premium.Q: When does floating beat fixing for five years?

Ans: Floating can work if you plan to repay within eighteen months or expect base rates to drop faster than spreads widen. Budget for swings: a one-point move on a five-million-dollar loan adds about 4 200 dollars in yearly interest.Q: What happens if I prepay a five-year fixed loan early?

Ans: Most lenders charge yield maintenance or swap breakage to stay whole. Costs peak early in the term. If you foresee a sale, ask for a step-down or sliding-scale prepay; it can save six figures in equity.

Sources and further reading

We pulled every number in this guide from public reports you can check yourself. Start with these anchors:

- Five-year Treasury outlook — Monthly forecast tables with confidence bands from the Financial Forecast Center (updated October 2025).

- Basel III “Endgame” — Reuters, September 25, 2025, where Fed Governor Bowman said regulators will publish a revised rule by early 2026.

- CRE maturity wall — Trepp’s running tally of 2024–28 loan maturities (last updated July 2025) shows more than 2.8 trillion dollars coming due.

For a broader dashboard, bookmark the Federal Reserve’s Summary of Economic Projections, CREFC’s monthly CMBS loan-performance report, and CBRE’s semi-annual U.S. Cap-Rate Survey. Together, they track macro rates, credit spreads, and asset pricing, all handy reference points before you sign the next term sheet.