Life insurance serves as a financial safety net, providing peace of mind and protection for your loved ones when you’re no longer there to provide for them. Among the various types of life insurance available, term life insurance has emerged as one of the most popular and practical choices for families and individuals seeking affordable coverage.

Term life insurance offers temporary protection for a specific period, making it an ideal solution for people who need substantial coverage during their prime earning years without the complexity and higher costs associated with permanent insurance policies. Its straightforward nature, combined with significantly lower premiums compared to whole life insurance, has made it the go-to choice for young families, new homeowners, and anyone looking to protect their financial dependents.

This comprehensive guide will walk you through everything you need to know about term life insurance, from understanding how it works to determining the right coverage amount for your specific needs. We’ll explore the different types available, examine the benefits and limitations, and provide practical advice on choosing the right policy to protect your family’s financial future.

What Is Term Life Insurance?

Term life insurance is a type of life insurance that provides coverage for a specific period, typically ranging from 10 to 30 years. Unlike permanent life insurance policies such as whole life or universal life, term insurance is designed to be temporary, offering pure insurance protection without any cash value or investment component.

The fundamental difference between term and permanent life insurance lies in their structure and purpose. While whole life insurance combines insurance protection with a savings or investment element that builds cash value over time, term life insurance focuses solely on providing a death benefit to your beneficiaries if you pass away during the policy term. This simplified approach makes term insurance significantly more affordable, allowing you to secure higher coverage amounts for a fraction of the cost of permanent policies.

Common policy terms include 10, 15, 20, and 30 years, with 20-year terms being the most popular choice among consumers. The term length you choose should align with your financial obligations and the period during which your dependents would need financial support. For example, if you have young children, you might choose a 20 or 30-year term to ensure coverage until they become financially independent.

The policy is called “term” because it provides coverage for a predetermined term or period. Once this term expires, the coverage ends, and you have no further obligation to pay premiums. However, many policies offer renewal options, though typically at much higher rates based on your age at renewal.

How Does Term Life Insurance Work?

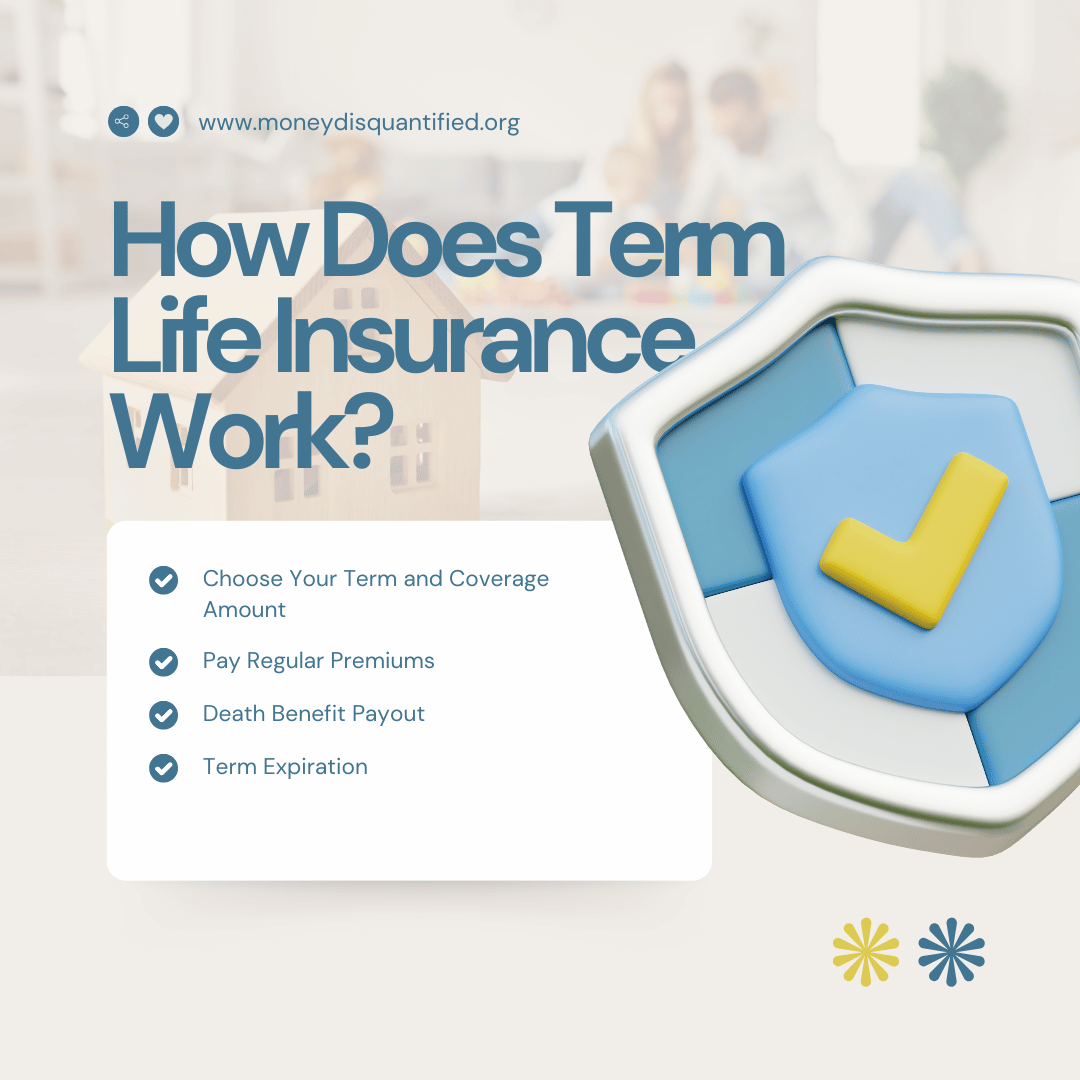

Understanding how term life insurance operates is straightforward, making it an accessible option for most people. The process begins when you decide on two crucial factors: the term length and the coverage amount you need.

Step 1: Choose Your Term and Coverage Amount You select a term length that matches your financial responsibilities timeline and determine how much coverage your beneficiaries would need. This decision should be based on your income, debts, and your family’s future financial needs.

Step 2: Pay Regular Premiums You’ll pay monthly or annual premiums throughout the policy term. These premiums remain level for most term policies, meaning your payment amount won’t change during the coverage period. As long as you continue paying premiums, your coverage remains active.

Step 3: Death Benefit Payout If you die during the policy term, your designated beneficiaries receive the full death benefit, typically tax-free. This money can be used to replace lost income, pay off debts, cover funeral expenses, or fund future needs like children’s education.

Step 4: Term Expiration If you outlive the policy term, the coverage simply ends. There’s no cash value to withdraw, no refund of premiums paid, and no payout to beneficiaries. The policy terminates, and you’re no longer covered.

Real-Life Example: Consider Sarah, a 30-year-old mother of two who purchases a 20-year, $500,000 term life insurance policy. She pays $25 monthly for coverage. If Sarah passes away in year 15 of her policy, her beneficiaries receive $500,000. However, if she lives beyond age 50 (when the 20-year term ends), the policy expires, and there’s no payout.

Optional Riders Many insurers offer additional features called riders that can enhance your basic term policy. Common riders include waiver of premium (continues coverage if you become disabled), accidental death benefit (doubles payout for accidental death), and child coverage (provides small amounts of coverage for children).

Types of Term Life Insurance

Term life insurance comes in several varieties, each designed to meet different needs and circumstances. Understanding these options helps you choose the most appropriate type for your situation.

Level Term Insurance This is the most common and popular type of term insurance. Level term policies maintain fixed premiums and death benefits throughout the entire term. Whether you’re in year one or year twenty of your policy, your monthly payment and coverage amount remain constant. This predictability makes budgeting easier and ensures your coverage won’t unexpectedly become more expensive.

Decreasing Term Insurance With decreasing term policies, your death benefit gradually reduces over time while premiums typically remain level. This type is often used for mortgage protection, where the coverage amount decreases along with your outstanding mortgage balance. The logic is that as you pay down debt, you need less insurance coverage to protect your family from that specific obligation.

Renewable Term Insurance Renewable term policies allow you to extend your coverage at the end of the term without requiring a new medical exam or health questionnaire. While this provides continuity of coverage, renewal typically comes at significantly higher premium rates based on your age at renewal. This option is valuable if your health has deteriorated and you couldn’t qualify for a new policy elsewhere.

Convertible Term Insurance This type allows you to convert your term policy to permanent life insurance (like whole life) within a specified period, usually without medical underwriting. Conversion can be valuable if your financial situation changes and you decide you need permanent coverage. However, the converted policy will have higher premiums reflecting the permanent insurance costs.

Benefits of Term Life Insurance

Term life insurance offers numerous advantages that make it the preferred choice for many individuals and families seeking life insurance protection.

Affordability The most significant advantage of term life insurance is its cost-effectiveness. Because it provides pure insurance protection without cash value accumulation, term policies can be 10-20 times less expensive than comparable whole life policies. This affordability allows you to purchase higher coverage amounts within your budget, ensuring adequate protection for your family.

Simplicity and Transparency Term life insurance is straightforward to understand. You pay premiums, and if you die during the term, your beneficiaries receive the death benefit. There are no complex investment components, fluctuating cash values, or confusing policy mechanics to navigate. This transparency makes it easier to compare policies and understand exactly what you’re purchasing.

Ideal for Temporary Needs Many financial obligations are temporary, making term insurance perfectly suited for these needs. Whether you’re paying off a mortgage, raising children, or supporting aging parents, term insurance can provide protection during these specific periods when your financial responsibilities are highest.

High Coverage for Low Cost Term insurance allows you to secure substantial coverage amounts at relatively low premiums, especially when you’re young and healthy. A healthy 30-year-old might secure $500,000 in coverage for less than $30 monthly, providing significant financial protection during peak earning and responsibility years.

The flexibility of term length options also allows you to match your coverage period to your specific needs, whether that’s a 10-year business loan or 30 years of child-rearing responsibilities.

Downsides and Limitations

While term life insurance offers many benefits, it’s important to understand its limitations to make an informed decision about whether it’s right for your situation.

No Cash Value Component Unlike permanent life insurance, term policies don’t build cash value that you can borrow against or withdraw. Every premium payment goes toward insurance protection, and if you outlive the policy term, there’s no financial return on your investment. This means you won’t have access to any accumulated value during your lifetime.

Coverage Ends After Term Once your term expires, your coverage terminates completely. If you still need life insurance beyond the original term, you’ll need to purchase a new policy, likely at much higher rates due to your increased age and potential health changes.

Renewal Costs Can Be Prohibitive While many term policies offer renewal options, the costs can be dramatically higher. Renewal rates are based on your age at renewal and current health status, often making continued coverage unaffordable for many policyholders.

No Payout for Survivors Statistics show that most term life insurance policies expire without ever paying a death benefit. If you outlive your policy term, there’s no payout to your beneficiaries, which some people view as “lost” premium payments, though this perspective overlooks the valuable protection provided during the coverage period.

Who Should Buy Term Life Insurance?

Term life insurance is particularly well-suited for specific groups of people whose financial situations align with its temporary nature and affordability.

Young Families with Children Parents with dependent children represent the ideal candidates for term life insurance. The coverage can replace lost income, fund children’s education, and maintain the family’s standard of living if a parent dies. A 20 or 30-year term often provides protection until children reach financial independence.

Single Parents Single parents face unique financial pressures and responsibilities. Term life insurance can ensure that children’s needs are met, including housing, education, and daily expenses, if the sole income provider dies. The affordable premiums make it accessible even on a single income.

Homeowners with Mortgages New homeowners often benefit from term life insurance to protect their families from mortgage obligations. The coverage can pay off the mortgage, allowing survivors to remain in the family home without the financial burden of monthly payments.

Anyone with Financial Dependents If others rely on your income for support, whether children, aging parents, or a spouse, term life insurance can provide crucial financial protection. This includes breadwinners in single-income households and primary earners in dual-income families.

People Seeking Affordable Protection Individuals who need substantial coverage but have limited budgets for insurance premiums find term life insurance particularly attractive. Young professionals, recent graduates, and those early in their careers can secure meaningful protection at costs that fit their financial situation.

How Much Coverage Do You Need?

Determining the appropriate amount of term life insurance coverage requires careful consideration of your family’s financial needs and obligations.

The 10x Rule A commonly cited guideline suggests purchasing coverage equal to 10 times your annual income. While this provides a starting point, your actual needs may vary significantly based on your specific circumstances. A person earning $50,000 annually might need $500,000 in coverage, but this rule doesn’t account for existing savings, debt levels, or specific family needs.

Factors to Consider

Income Replacement: Calculate how many years your family would need financial support, and multiply that by your annual income. Consider whether your spouse works and how much of your income needs replacement.

Debt Obligations: Include mortgage balances, credit card debt, student loans, and other financial obligations that would burden your family. Your life insurance should be sufficient to eliminate these debts.

Children’s Education: Estimate future education costs for your children, including college expenses that continue to rise above inflation rates.

Final Expenses: Factor in funeral and burial costs, which can range from $7,000 to $15,000 or more, plus any immediate expenses your family might face.

Online calculators provided by insurance companies and financial websites can help you work through these calculations systematically. These tools consider multiple factors and provide personalized recommendations based on your specific financial situation.

How Much Does Term Life Insurance Cost?

The cost of term life insurance varies significantly based on several key factors, but it remains remarkably affordable for most healthy individuals.

Primary Cost Factors

Age: Younger applicants pay significantly lower premiums. A 25-year-old might pay $15 monthly for $250,000 in coverage, while a 45-year-old might pay $45 for the same policy.

Health Status: Your overall health, including medical history, current conditions, and lifestyle factors like smoking, dramatically impact premiums. Smokers typically pay 2-3 times more than non-smokers.

Coverage Amount: Higher death benefits result in higher premiums, though the per-dollar cost often decreases with larger policies.

Term Length: Longer terms generally cost more annually but provide rate guarantees for extended periods.

Sample Costs A healthy 30-year-old non-smoking male might expect to pay approximately $20-30 monthly for $500,000 in 20-year term coverage. A 40-year-old woman in good health might pay $30-40 monthly for the same coverage.

Medical Exam vs. No-Exam Policies Traditional policies require medical exams, including blood tests, urine samples, and sometimes EKGs. No-exam policies offer convenience but typically cost 25-50% more and may offer lower maximum coverage amounts.

Money-Saving Tips Purchase coverage while young and healthy, maintain a healthy lifestyle, compare quotes from multiple insurers, and consider buying coverage in round numbers (like $250,000 instead of $247,000) as insurers often offer better rates for standard amounts.

How to Choose the Right Policy

Selecting the appropriate term life insurance policy requires careful evaluation of your needs, financial situation, and long-term goals.

Evaluate Your Financial Situation Start by assessing your current financial obligations, including mortgage payments, debt service, and family expenses. Consider how these needs might change over time and whether your coverage should remain level or could decrease as debts are paid off.

Determine Appropriate Term Length Choose a term that covers your period of greatest financial responsibility. If you have young children, a 20-30 year term might be appropriate. If you’re primarily concerned about mortgage protection, a 15-20 year term might suffice.

Compare Multiple Insurers Premium rates can vary significantly between insurance companies for identical coverage. Obtain quotes from at least three to five insurers to ensure you’re getting competitive rates. Online comparison tools can streamline this process.

Evaluate Insurer Financial Strength Choose insurers with strong financial ratings from agencies like A.M. Best, Moody’s, or Standard & Poor’s. An A+ rating or higher indicates financial stability and the ability to pay claims. Research customer service ratings and complaint ratios through your state insurance department.

Consider Policy Features Look for policies with conversion options if you think you might need permanent coverage later. Examine renewal provisions and any included riders. Some policies offer additional benefits like coverage for terminal illness or waiver of premium for disability.

Frequently Asked Questions About Term Life Insurance

Can I cancel my term life insurance policy? Yes, you can cancel your term life insurance policy at any time without penalty. Simply stop paying premiums, and the policy will lapse. However, you won’t receive any refund of premiums paid, and you’ll lose your coverage immediately.

Can I get a refund if I cancel my policy? Most term life insurance policies don’t provide refunds if you cancel. Some insurers offer return-of-premium term policies that refund premiums if you outlive the term, but these policies cost significantly more than standard term insurance.

What happens if I miss a premium payment? Most policies include a grace period, typically 30 days, during which you can make late payments without losing coverage. If you don’t pay within the grace period, your policy lapses, and coverage ends. Some insurers offer automatic premium loans or other options to prevent accidental lapses.

What if I need more coverage later? If you need additional coverage, you’ll typically need to apply for a new policy, which will require new medical underwriting and higher premiums based on your current age. Some policies offer guaranteed insurability riders that allow you to purchase additional coverage at specific intervals without medical exams.

Can I convert my term policy to permanent insurance? Many term policies include conversion privileges that allow you to convert to permanent life insurance within a specified period, usually without medical underwriting. The converted policy will have higher premiums reflecting permanent insurance costs, but this option can be valuable if your health has declined.

Conclusion

Term life insurance represents an excellent solution for individuals and families seeking affordable, straightforward life insurance protection. Its simplicity, cost-effectiveness, and flexibility make it particularly well-suited for young families, homeowners, and anyone with temporary financial obligations or dependents who need protection.

The key to maximizing term life insurance’s benefits lies in understanding your specific needs, choosing appropriate coverage amounts and term lengths, and selecting a financially stable insurer. While term insurance has limitations, including the lack of cash value and temporary coverage, these characteristics also contribute to its affordability and simplicity.

For most people, especially those in their prime earning years with significant financial responsibilities, term life insurance offers the best combination of substantial protection and affordability. By carefully evaluating your needs and comparing options from multiple insurers, you can secure coverage that provides peace of mind and financial security for your loved ones.

Take the time to assess your family’s financial needs, explore your options, and consider speaking with a licensed insurance professional who can help you navigate the selection process and ensure you choose the right policy for your unique situation.

Ready to protect your family’s future? Compare term life insurance quotes today and take the first step toward securing your loved ones’ financial well-being.