An auto equity loan allows you to borrow money against the value of your vehicle, using your car as collateral. Think of it as a way to unlock the cash tied up in your car without having to sell it. You get to keep driving your vehicle while accessing funds for whatever you need.

When you have an auto equity loan, your car serves as security for the lender. This means if you can’t make your payments, the lender has the right to take your car to recover their money. But if you make payments on time, you keep your car and get access to cash at potentially lower interest rates than credit cards or personal loans.

The amount you can borrow depends on how much equity you have in your vehicle. Equity is simply the difference between what your car is worth and what you still owe on any existing car loan. For example, if your car is worth $15,000 and you owe $5,000 on your current loan, you have $10,000 in equity that you might be able to borrow against.

How Auto Equity Loans Work

Auto equity loans work by turning your car’s value into available cash. Here’s a detailed breakdown of the process:

Step 1: Determine Your Car’s Equity. First, you need to figure out how much equity you have in your vehicle. Start by finding your car’s current market value using resources like Kelley Blue Book, Edmunds, or similar valuation tools. Then subtract any amount you still owe on existing car loans. The result is your available equity.

For instance:

- Car’s market value: $20,000

- Outstanding loan balance: $8,000

- Available equity: $12,000

Most lenders will let you borrow between 50% to 90% of your available equity, depending on your creditworthiness and their specific policies.

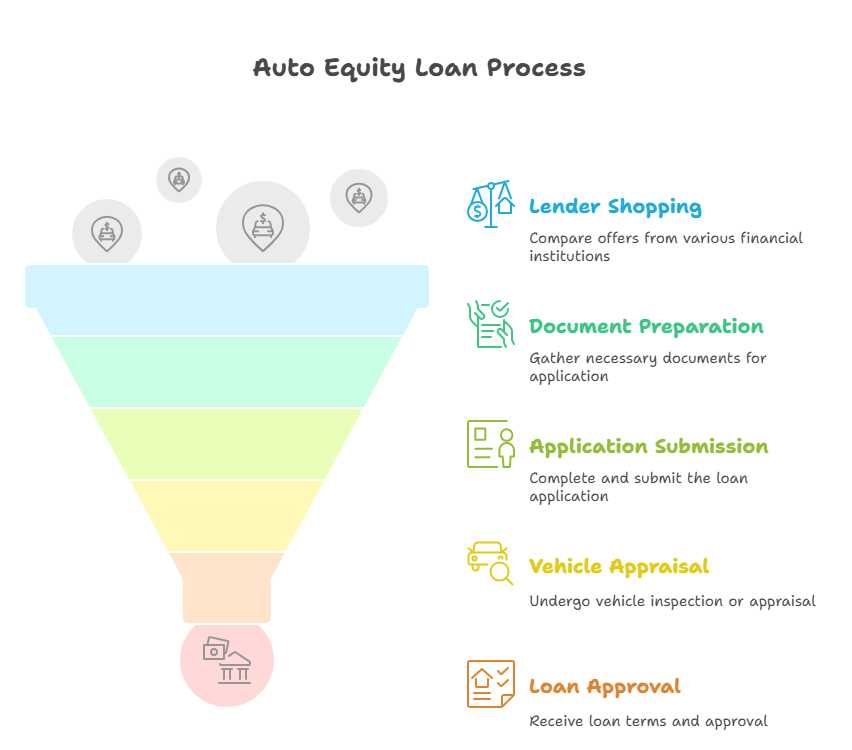

Step 2: Shop for Lenders. Auto equity loans are offered by various financial institutions, including:

- Credit unions (often offer the best rates for members)

- Traditional banks

- Online lenders

- Specialized auto loan companies

Each lender has different requirements, interest rates, and terms, so it pays to shop around and compare offers.

Step 3: Gather Required Documents Before applying, prepare these common documents:

- Vehicle title (must be in your name)

- Valid driver’s license or state ID

- Proof of income (pay stubs, tax returns, bank statements)

- Proof of insurance (comprehensive and collision coverage required)

- Vehicle registration

- Recent photos of your car (interior and exterior)

Step 4: Complete the Application The application process typically involves:

- Filling out personal and financial information

- Providing vehicle details (make, model, year, mileage, condition)

- Submitting required documentation

- Allowing a vehicle inspection or appraisal

Step 5: Vehicle Appraisal Most lenders will want to verify your car’s condition and value through:

- In-person inspection at their location

- Mobile appraisal at your home or workplace

- Photos and detailed vehicle information (for online lenders)

Step 6: Loan Approval and Funding Once approved, you’ll receive:

- Loan terms including interest rate, monthly payment, and repayment period

- Information about any additional fees

- Instructions for accessing your funds

Funding can happen quickly – sometimes within hours for online lenders or the same day for local institutions. The money is typically deposited directly into your bank account.

Step 7: Repayment You’ll make regular monthly payments that include both principal and interest. The repayment term usually ranges from 12 to 60 months, depending on the loan amount and lender policies. During this time, you continue driving your car normally while the lender holds a lien on the title.

How to Get an Auto Equity Loan

Getting an auto equity loan involves several key steps and requirements. Here’s what you need to know:

Eligibility Requirements Most lenders require:

- You must own the vehicle outright OR have significant equity in it

- The car must be titled in your name

- Vehicle must be less than 10-15 years old (varies by lender)

- Car must be in good working condition

- You must have steady income to support loan payments

- Valid driver’s license and insurance

- Some lenders have minimum income requirements

Improving Your Chances of Approval To increase your likelihood of getting approved and securing better terms:

- Check Your Credit Score: While auto equity loans are secured by your vehicle, your credit score still matters for interest rates and loan terms. Higher credit scores typically mean lower interest rates.

- Gather Strong Documentation: Have all required paperwork organized and ready. This shows lenders you’re serious and helps speed up the process.

- Consider a Co-signer: If your credit isn’t great, having a co-signer with good credit can help you qualify and get better terms.

- Shop Multiple Lenders: Different lenders have varying requirements and rates. Credit unions often offer the most competitive rates for their members.

- Be Realistic About Loan Amount: Don’t ask to borrow the maximum possible. Requesting 70-80% of your equity instead of 90% can improve approval odds.

The Application Process Timeline

- Day 1: Submit application and documents

- Day 1-2: Vehicle appraisal/inspection

- Day 2-3: Underwriting and approval decision

- Day 3-5: Funding (can be same-day with some lenders)

Questions to Ask Potential Lenders Before committing, ask:

- What’s the interest rate and APR?

- Are there origination fees or other upfront costs?

- What’s the repayment term?

- Are there prepayment penalties?

- What insurance coverage is required?

- What happens if I want to sell my car before the loan is paid off?

Pros and Cons of an Auto Equity Loan

Like any financial product, auto equity loans have both advantages and disadvantages. Understanding these can help you make an informed decision.

Benefits of Auto Equity Loans

Quick Access to Funds Auto equity loans are known for fast processing and funding. Unlike traditional personal loans that might take weeks, many auto equity lenders can approve and fund loans within 24-48 hours. This makes them ideal for emergency expenses or time-sensitive financial needs.

Lower Interest Rates Because your vehicle secures the loan, lenders face less risk and can offer lower interest rates compared to unsecured options like credit cards or personal loans. While rates vary based on your credit score and the lender, auto equity loans typically offer rates between 6% to 18%, compared to credit card rates that can exceed 25%.

Easier Qualification The collateral aspect makes these loans more accessible to people with less-than-perfect credit. Even if you’ve been denied for unsecured loans, you might qualify for an auto equity loan if you have sufficient vehicle equity and income to make payments.

Keep Your Vehicle Unlike selling your car for cash, an auto equity loan lets you access your vehicle’s value while continuing to drive it daily. This is crucial for people who need their car for work, family responsibilities, or lack access to public transportation.

Flexible Use of Funds Most lenders don’t restrict how you use the loan proceeds. Common uses include:

- Medical bills or dental work

- Home repairs or improvements

- Debt consolidation

- Business expenses

- Emergency expenses

- Education costs

Potential Credit Building Making on-time payments can help improve your credit score over time, especially if you have limited credit history or past credit challenges.

Potential Drawbacks and Risks

Risk of Vehicle Repossession The biggest risk is losing your car if you can’t make payments. Unlike missing a credit card payment, defaulting on an auto equity loan can leave you without transportation, which could impact your ability to work and earn income to resolve the financial problem.

Limited Borrowing Power You can only borrow based on your vehicle’s equity, which might not be enough for large expenses. If you need $25,000 but only have $10,000 in car equity, this option won’t meet your needs.

Vehicle Depreciation Risk Cars lose value over time, sometimes quickly. If you borrow a large percentage of your equity and your car depreciates faster than you pay down the loan, you could end up owing more than the car is worth (called being “upside down” or having negative equity).

Insurance Requirements Lenders typically require comprehensive and collision coverage throughout the loan term. If you currently only carry liability insurance, this additional coverage will increase your monthly expenses.

Additional Fees and Costs Beyond interest, you might pay:

- Origination fees (1-5% of loan amount)

- Appraisal fees ($100-300)

- DMV lien recording fees

- Late payment fees

- Prepayment penalties (some lenders)

Impact on Future Vehicle Decisions With a lien on your title, you can’t sell or trade your vehicle without first paying off the auto equity loan. This can limit your flexibility if your transportation needs change or if you want to upgrade to a different vehicle.

Temptation to Overborrow Easy access to cash against your vehicle’s value might tempt you to borrow more than you actually need or can comfortably repay, potentially creating a cycle of debt.

Auto Equity Loan Alternatives

Before committing to an auto equity loan, consider these alternative options that might better suit your situation:

Unsecured Personal Loans

Personal loans don’t require collateral, meaning your vehicle isn’t at risk if you can’t make payments. While interest rates are typically higher than secured loans, they offer several advantages:

Benefits:

- No risk of losing your car

- Fixed interest rates and payments

- Flexible use of funds

- No vehicle age or condition requirements

- Faster approval process (no vehicle appraisal needed)

Drawbacks:

- Higher interest rates (typically 8-25% depending on credit)

- Stricter credit requirements

- Lower loan amounts for those with poor credit

- Shorter repayment terms in some cases

Best for: People with good to excellent credit who want to avoid putting their vehicle at risk.

Cash-Out Auto Refinancing

This involves replacing your existing car loan with a new, larger loan and taking the difference in cash. For example, if you owe $10,000 on your car but it’s worth $20,000, you might refinance for $15,000 and pocket $5,000.

Benefits:

- Often lower interest rates than equity loans

- One car payment instead of two

- May improve your loan terms if rates have dropped

- Less risky than adding a second lien

Drawbacks:

- Only works if you have an existing car loan

- May extend your repayment period

- Increases your total debt on the vehicle

- Resets the loan term, potentially increasing total interest paid

Best for: People with existing car loans who want cash and potentially better loan terms.

Home Equity Loan or HELOC

If you own a home with equity, you might access cash through a home equity loan or Home Equity Line of Credit (HELOC).

Benefits:

- Generally lowest interest rates available

- Tax-deductible interest in some cases

- Larger borrowing amounts possible

- Longer repayment terms

- No vehicle-related restrictions

Drawbacks:

- Your home becomes collateral

- Longer application and approval process

- Closing costs and fees

- Risk of foreclosure if you default

- Requires homeownership with sufficient equity

Best for: Homeowners with substantial home equity who need large amounts of cash and want the lowest possible interest rates.

Credit Cards

For smaller amounts or short-term needs, credit cards might be an option, especially if you can take advantage of promotional offers.

Benefits:

- Immediate access to funds

- No collateral required

- Promotional 0% APR periods available

- Rewards programs

- Building credit with responsible use

Drawbacks:

- High interest rates (typically 18-29%)

- Can lead to minimum payment trap

- Easy to overspend

- Variable interest rates

- Potential for significant debt accumulation

Best for: Small amounts needed short-term, or people who can pay off balances quickly.

Family and Friends

Borrowing from people you know can offer flexibility and potentially better terms than traditional lenders.

Benefits:

- No interest or low interest rates

- Flexible repayment terms

- No credit check required

- No risk of repossession or foreclosure

Drawbacks:

- Can strain relationships if problems arise

- No legal protections

- May create awkward family dynamics

- No credit-building benefits

- Limited amounts typically available

Best for: People with financially stable family members or friends willing to lend money.

401(k) Loans

If you have a 401(k) retirement account, you might be able to borrow against it.

Benefits:

- No credit check required

- Relatively low interest rates

- You pay interest to yourself

- No taxes or penalties if repaid on time

- Fast access to funds

Drawbacks:

- Reduces retirement savings

- Must repay if you leave your job

- Lost investment growth opportunity

- Potential taxes and penalties if not repaid

- Not available with all employers

Best for: People with substantial 401(k) balances who can repay the loan reliably.

Peer-to-Peer Lending

Online platforms connect borrowers with individual investors willing to fund loans.

Benefits:

- Competitive interest rates for good credit

- Flexible terms

- Online application process

- May approve borrowers traditional banks won’t

Drawbacks:

- Still requires good credit for best rates

- Origination fees common

- Not available in all states

- Less regulation than traditional banks

Best for: People with decent credit who want to explore non-traditional lending options.

The Takeaway

An auto equity loan can be a useful financial tool when you need cash quickly and have significant equity in your vehicle. The key is understanding both the benefits and risks before making a decision.

Auto equity loans work best when:

- You need money quickly for a legitimate financial need

- You have substantial equity in a reliable vehicle

- You have steady income to support loan payments

- You understand and accept the risk of potential vehicle repossession

- Other financing options aren’t available or offer worse terms

Consider alternatives when:

- You have good credit and qualify for unsecured personal loans

- You’re not comfortable risking your vehicle

- You need more money than your car equity allows

- You have access to lower-cost options like home equity

- The loan would strain your budget significantly

Before applying for any loan:

- Calculate exactly how much you need – Don’t borrow more than necessary just because you can.

- Shop around – Compare rates, terms, and fees from multiple lenders including credit unions, banks, and online lenders.

- Read the fine print – Understand all fees, insurance requirements, and what happens if you want to pay off early or sell your vehicle.

- Create a repayment plan – Make sure you can comfortably afford the monthly payments along with your other expenses.

- Have a backup plan – Consider what you’ll do if your financial situation changes and you can’t make payments.

- Consider the total cost – Look at the total amount you’ll pay over the life of the loan, not just the monthly payment.

Red flags to avoid:

- Lenders who don’t verify your income or ability to repay

- Extremely high interest rates (over 25%)

- Pressure to sign immediately without reviewing terms

- Requests for upfront fees before loan approval

- Lenders who aren’t properly licensed in your state

Remember, an auto equity loan is a serious financial commitment that puts your vehicle at risk. While it can provide quick access to cash at reasonable rates, make sure you fully understand the terms and have confidence in your ability to repay the loan on schedule. If you’re unsure, consider speaking with a financial advisor or credit counselor who can help you evaluate your options and make the best decision for your situation.

The most important thing is to borrow responsibly and only take on debt you can realistically repay. Your vehicle is likely essential for your daily life and livelihood, so protect it by making informed financial decisions and keeping up with your loan payments.